A mulled wine here, a business dinner there, and all the Christmas parties with friends and family. So much to do and so little time. But there is something that you should definitely do in December: make sure you have paid into your pillar 3a account by the end of the year. Our checklist will save you money – and time.

What are you giving yourself for Christmas? We have an idea that’s great for you and your financial future. Investing in a tax-qualified 3rd pillar lets you save for what lies ahead. Check with your pillar 3a when the last possible date for a deposit is, and be sure to write it in your calendar.

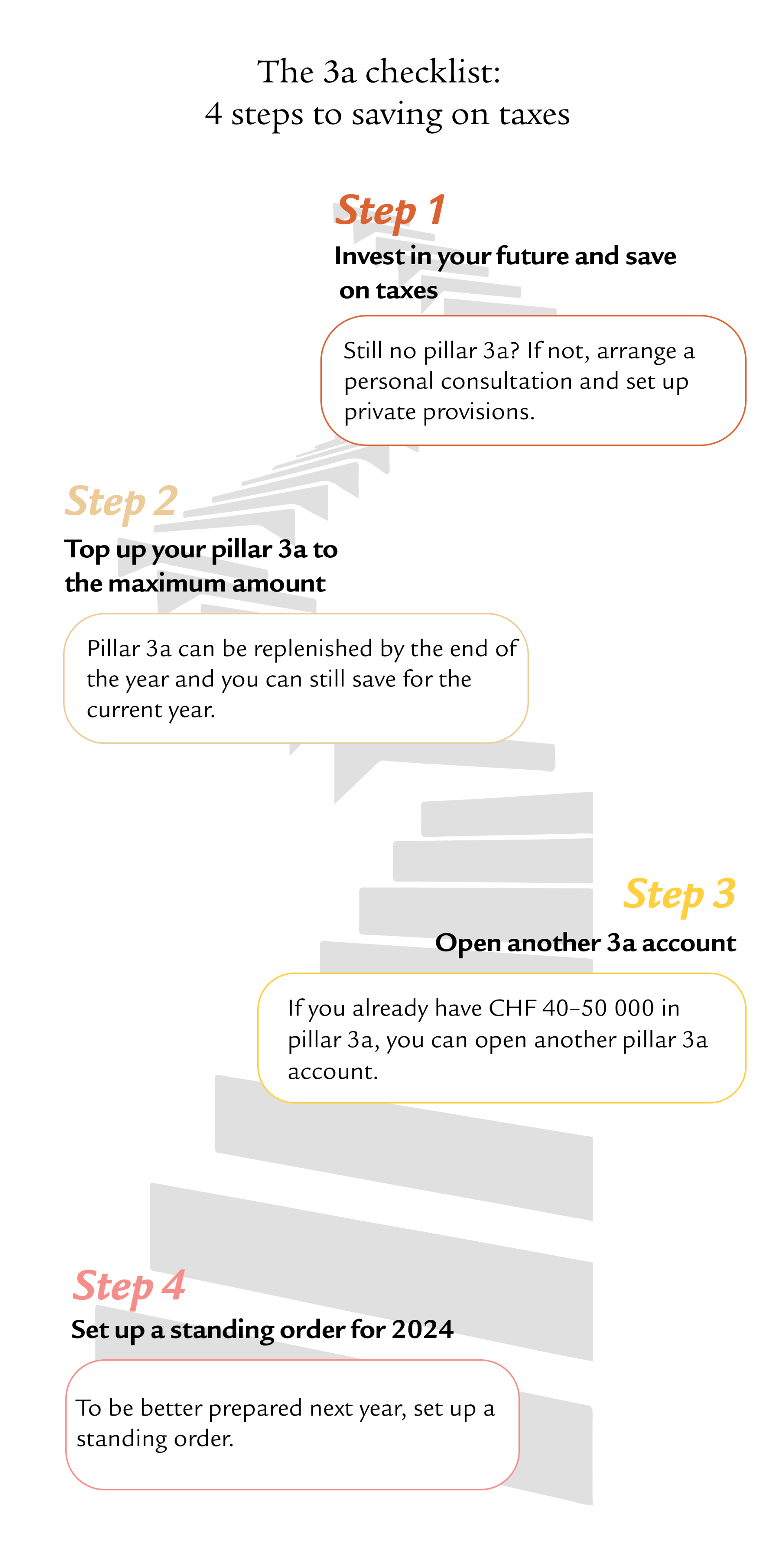

Step 1

Invest in your future and save on taxes

Do you already have a 3rd pillar account? If not, you should contact one of our advisors as soon as possible to set up your personal pillar 3a account.

Pillar 3a not only allows you to provide for your future, it also allows you to benefit from tax advantages. Each year, you can deduct the full amount you pay into your pillar 3a from your taxable income.

Tax calculator

Use our tax savings calculator to find out how much tax you can save with a pillar 3a.

Step 2

Top up your pillar 3a to the maximum amount

If you have already paid something into your existing 3rd pillar, you can top it up to the maximum amount by the end of December. If you are in employment and a member of a pension fund, this amounts to CHF 7056 in 2023. If you are self-employed without a pension fund, you can pay in up to 20% of your net income up to a maximum of CHF 35 280.

You can fully deduct any amounts paid into your retirement provisions from your taxable income. This allows you to save up to CHF 2500 a year, depending on your income and canton.

You don’t have this much money left over or you would rather spend it on something else? No problem, it’s worth paying in even smaller amounts over the long term. You can find out more in our helpful guide: Are you saving with pillar 3a?Start the payments at a young age

Step 3

Open another 3a account

If you already have CHF 40 000–50 000 in your pillar 3a account, it would be worth opening another pillar 3a account. However, it depends on whether and how your retirement provisions are invested. Why is this? It is not possible to make partial withdrawals from a 3a account (for example, because you want to become self-employed, emigrate, buy a house or take early retirement). What’s more, depending on the canton, you can save a lot of tax when you retire by gradually releasing money from different accounts. If you have more than one account, you are more flexible when it comes to withdrawing money.

In addition, half of all 3a savers have already spread their assets across at least two or more accounts.

Step 4

Set up a standing order for 2023

Would you like to be better prepared next year? Then set up a standing order now. A standing order will take a certain amount each month, which you can then invest and let work for you. This makes it easier to plan your budget. Furthermore, the key factor for the success of any long-term investment such as your 3a is not the timing of the investment (market timing), but the time in the market. So it’s not worth waiting around. And by making consistent monthly investments in your 3a, you will become less dependent on market fluctuations.

If you are in employment and a member of a pension fund, the maximum amount is CHF 7056 in 2023. As a self-employed person without a pension fund, you can pay in a maximum of CHF 35 280. This would amount to CHF 588 a month for employees or CHF 2940 for the self-employed.

Pillar 3a: answers to the nine top questions

Living a self-determined life when you’re older, securing your financial future, making your greatest wishes come true – who doesn’t dream of living life to the fullest even in retirement, while benefiting from tax advantages now? Saving with pillar 3a can make this dream come true. Swiss Life answers the most important questions related to this topic.

Set up a pillar 3a account.

Obtain free pillar 3a advice with no strings attached.